$META is a money printer, and the only reason it’s cheap is that investors remain hesitant about what founder and CEO Mark Zuckerberg keeps spending all the printed cash on: things the market is either unsure of or has flat-out rejected, like the metaverse. The spending is a real issue, because it is massive. But the potential on the other side of it is also uncapped.

Take out the spending that hasn’t worked, value the businesses underneath it, and the apps alone are worth more than what the whole company trades for on a per-share basis today. Then, and only then, do you put a price on the AI bet, the thing a lot of people, not just Zuckerberg, are obviously all in on, and the thing that could in theory double or triple this stock. You’re getting that part for free.

The complaints about Meta’s capital allocation are fair. Zuckerberg should not have done the metaverse, and honestly the company should change its umbrella name back to Facebook, switch the ticker back to $FB, and put Reality Labs behind it. Oculus cost $2 billion in 2014 and has turned into more than $80 billion of cumulative Reality Labs losses since 2020, with no real end in sight. About $19 billion of that came in 2025 alone. (The one real exception is the Ray-Ban Meta glasses, which are actually selling: sales tripled year over year, and the new display model sold out in 48 hours. They might be the first Reality Labs product that turns into a real business. But Quest and the rest of the metaverse keep the segment deep in the red regardless.) Libra died. Portal died. On and on. So the hesitancy is understandable. But keep it in perspective: you could put every failed project Meta has ever shipped in a blender, and it still wouldn’t come close to the capex they’re spending in a single year to build out AI.

Here’s the other side, though, and it’s the side I think matters more, and it’s why I’m writing this as a believer in Meta. Zuckerberg is a real risk-taker and a real visionary, and he’s doing it with cash flow most companies can only dream about. Jeff Bezos has a line I think about constantly here, from his 2015 letter to Amazon shareholders: in baseball, no matter how well you connect, the most you can score on one swing is four runs. But in business, every once in a while, you step up to the plate and score 1,000. Zuckerberg swings for 1,000 every time. He strikes out plenty. But Instagram was a 1,000-run swing, and you only need a couple of those.

Instagram cost $1 billion and is worth roughly 840 times that today, maybe more if it stood on its own. WhatsApp at $19 billion looked crazy and looks free now. The wins crush the losses, and it’s not close, and the engine underneath all of it, the best advertising algorithms ever built, keeps getting stronger no matter what the company wastes on the side. If AI works out, Meta is a leader. If it doesn’t, it hurts, but it doesn’t kill the company. Just look at the money they have. That asymmetry is the entire trade.

A Money Printer

In 2025 Meta reported a mammoth $201 billion in revenue, up 22% year over year, with $83.3 billion of operating income and $60.5 billion of net income. (Quick footnote so nobody emails me: that $60.5 billion was actually down a touch from $62.4 billion in 2024, but only because of a one-time $16 billion tax charge from the new tax law in Q3. Strip it out and earnings grew right in line with revenue. It’s also why the trailing P/E looks like ~25x while the forward multiple sits below 20.) And 2026 has started even faster: Q1 revenue, reported at the end of April, came in at $56.3 billion, up 33% year over year. 3.58 billion people use a Meta app every single day, more than four in ten humans alive. That’s the part nobody can take away.

The trick to understanding this stock is to separate the two companies bolted together inside it. The first is the set of apps those 3.58 billion people open every day: Facebook, Instagram, WhatsApp, and Threads (that last one nobody really uses yet). The apps are basically the entire revenue line, $199 billion of it, at a frankly hysterical 52% operating margin. Fifty-two percent. That is a software-grade margin on an advertising business at the scale of the planet, and it still grows at double digits. The second company is Reality Labs, which did $2.2 billion in revenue and lost $19.2 billion. One of these is among the best businesses ever built. The other is a money pit.

Two numbers tell you the apps are getting stronger, not weaker. In 2025, ad impressions went up 12% and the price per ad went up 9%, at the same time. A business without a real moat couldn’t pull that off. So the question isn’t whether Meta has a moat. It clearly does. The question is how impenetrable it is, and my answer is: very.

Meta raised volume and price together, across half the world, and a big chunk of that 9% price increase is the AI doing the targeting. Some of the AI spend everyone’s so hesitant about is already paying for itself. You can see it right there in that 9%.

Instagram Is Bigger Than You Think

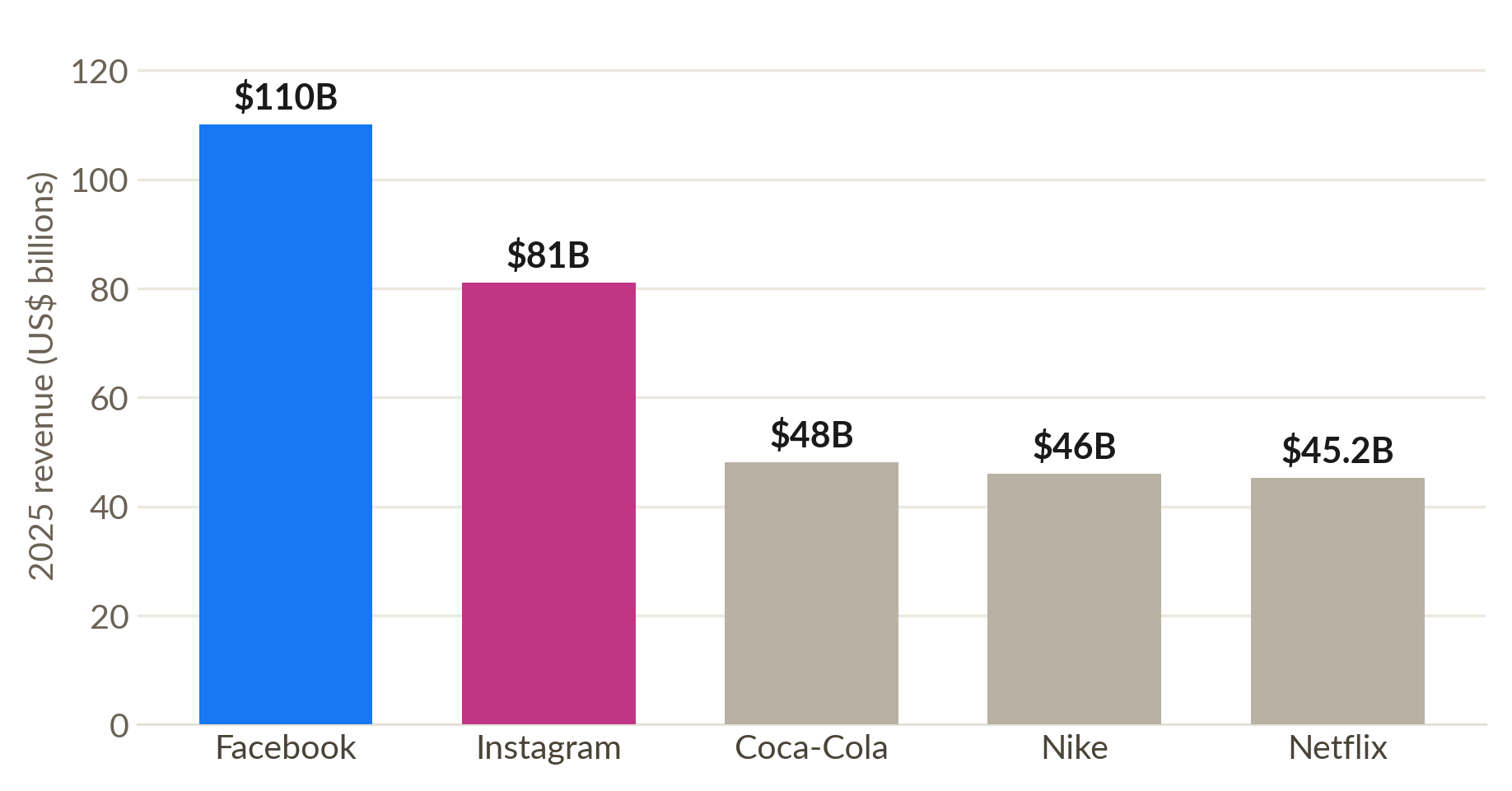

Netflix did about $45 billion in revenue last year. Nike did about $46 billion. Coca-Cola, about $48 billion. Instagram did roughly $81 billion, nearly double any one of them. People know Instagram is big. I’m not sure they know it out-earns each of those names, Netflix and Nike and Coke, while charging users nothing.

Figure 1: 2025 revenue. Netflix ($45.2B), Nike (~$46B), and Coca-Cola (~$48B) are disclosed. Facebook (~$110B) and Instagram (~$81B) are estimates. Meta doesn’t break out revenue per app, so I back into it from its disclosed ad revenue and eMarketer’s data showing Instagram passed 50% of Meta’s US ad revenue.

Meta doesn’t disclose revenue by app, so that $81 billion is an estimate, not a fact, but it’s a careful one, built off eMarketer’s data and landing in the $78–84 billion range that the people who model this for a living use. And if you’ve ever opened the app you know why it’s worth it: Instagram has the best recommendation algorithm ever made. It’s better than TikTok because it’s ranking against a logged-in account with your purchase history attached, so it knows what you’ll buy, not just what you’ll watch.

So what’s Instagram worth on its own? It runs at about the same 52% margin as the rest of the apps. Take a little off that, since a standalone Instagram would have to pay for some of what Meta currently shares across the whole company, put a growth multiple on the earnings, and you get to around $840 billion in the base case. The quick way to check it: Netflix trades at about 7.6 times its revenue, and it grows slower than Instagram with margins around 30% against the apps’ 52%. Put Netflix’s multiple on Instagram’s $81 billion and you get about $615 billion as a floor, before you pay anything for the faster growth and the extra twenty points of margin. Add a reasonable premium for both and you land comfortably north of $800 billion. Call it $840 billion, which is more than half of Meta’s entire $1.5 trillion market cap. One business out of four.

Simple Math

Facebook is a legacy app at this point, and everyone keeps trying to bury it, but it keeps growing. Here’s the part that trips people up: worldwide, Facebook still pulls in more ad revenue than Instagram, somewhere around $108 to $110 billion. Instagram only passed it in the US. But Facebook grows slower, so it earns a lower multiple, and that’s why it lands a little behind Instagram in this exercise, at roughly $770 billion on its own. More revenue, lower value, because of the growth gap. Then there’s WhatsApp: 3 billion users, barely monetized, only now starting to run ads. A network that big making a few dollars at most per user per year is either a failure or the biggest untapped asset in tech, and Meta’s history says they eventually flip the switch. Call it $150 billion, and that’s me being conservative. The math here isn’t hard to do yourself.

Add it up.

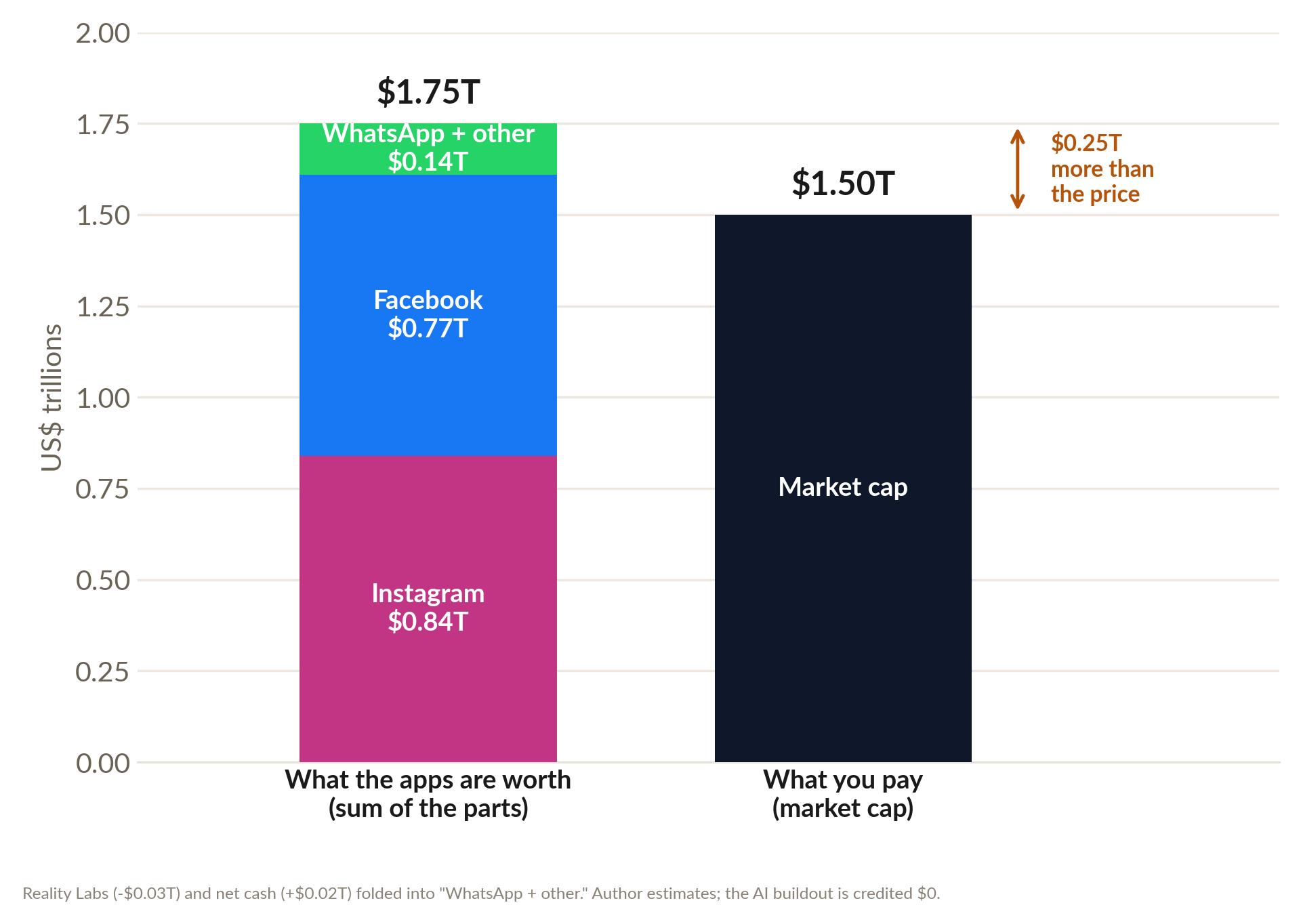

Figure 2: The apps add up to about $1.75 trillion (Instagram ~$840B, Facebook ~$770B, WhatsApp and the rest ~$140B net of Reality Labs), against a ~$1.50 trillion market cap. You’re paying about $0.25 trillion less than the parts are worth, with the AI buildout credited at zero. Source: my estimates; per-app figures modeled, segment totals disclosed.

So here’s the whole thesis in one number: the apps are worth more than the entire company. Meta closed the week at $593 a share (I’m publishing this on June 9th, so the price may have moved by the time you read it). At $593 you’re paying less than the advertising businesses are worth on their own, which means the market is throwing in the entire AI buildout, $125 to $145 billion a year of it, at less than zero. It isn’t paying a cent for that bet. If anything, it’s taking money off the stock for the cash the bet burns. Call that discount what it is: a Zuckerberg tax.

Run that to a per-share number and you get a range.

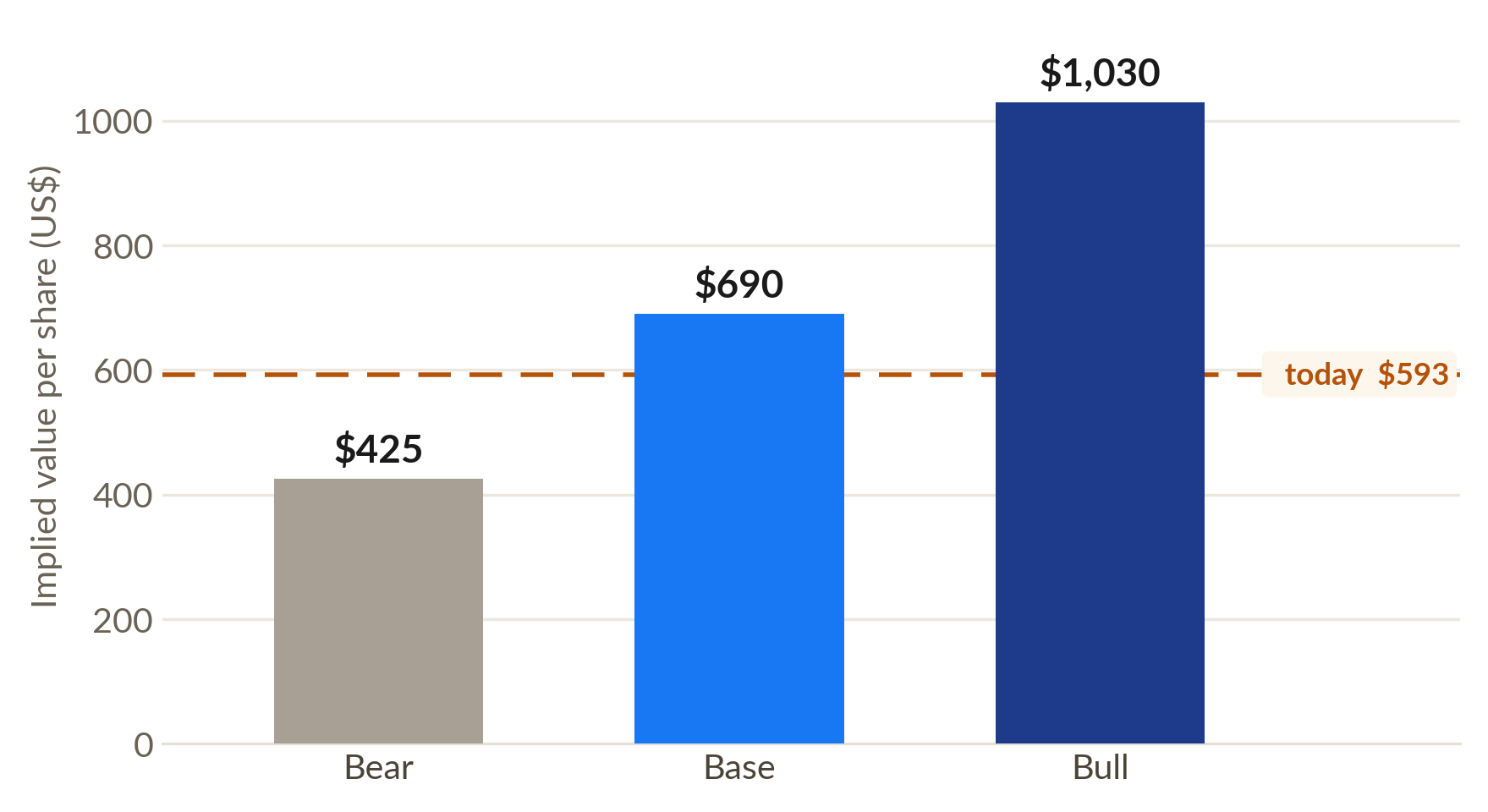

Figure 3: What the apps alone are worth per share: about $425 in a bear case, $690 base, $1,030 bull, against Friday’s $593 close. AI working is not in any of these numbers; it’s upside on top. Source: my analysis.

Base case is about $690 a share on the apps alone, roughly 16% above where it trades. The bull case at $1,030 doesn’t even need AI to work. It just needs the apps to trade like the pure advertising businesses they are, with WhatsApp finally switched on. The downside is around $425, which is what the apps are worth even in a genuinely bearish case.

When Management Bets on Itself

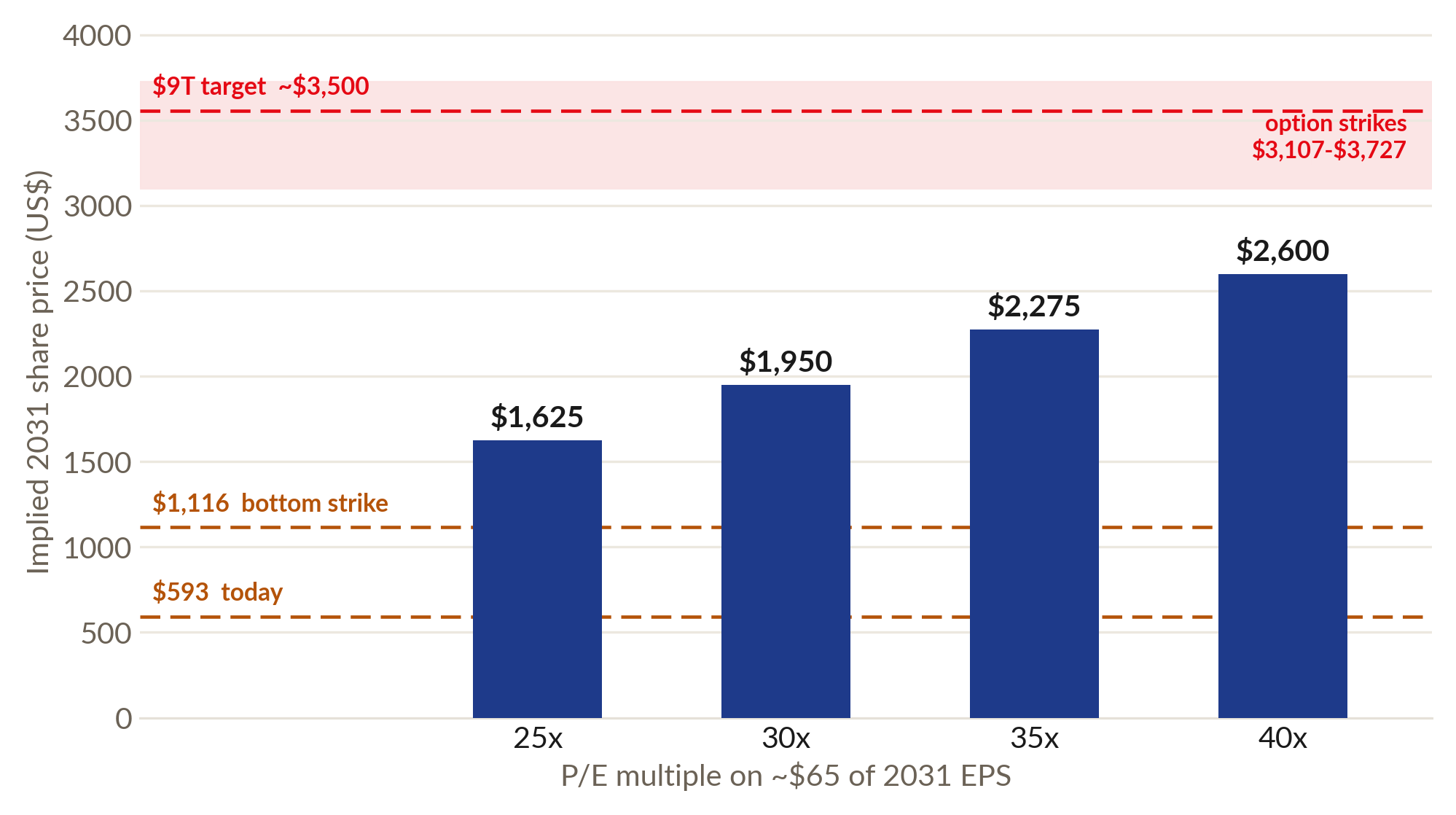

Here’s the thing that actually convinced me, and it’s been sitting in articles published over the past few months. In March of this year Meta handed its top six executives the first stock options it had granted since the 2012 IPO. The four most senior got 653,865 options apiece, the other two smaller grants on the same terms, at strike prices running from $1,116 a share all the way up to $3,727. The lowest strike doesn’t pay out until the stock nearly doubles. The highest doesn’t pay until Meta is a $9 trillion company, around $3,500 a share, about six times where it trades today.

Now run the earnings side. Stretch Meta’s profit out to 2031 and you land around $65 a share in earnings (that’s my number, since almost nobody on the Street publishes an estimate that far out). Here’s where the stock would trade at a range of P/E multiples on that $65, against where those strikes actually sit:

Figure 4: Implied 2031 share price at 25x–40x of an estimated ~$65 of 2031 earnings, against the executive strike ladder ($1,116 at the bottom, up to $3,727) and the $9T target (~$3,500). Even 40x earnings doesn’t reach the top of their own grants. Source: Meta filings, CNBC, Fortune; 2031 EPS is my estimate.

Look at the chart. Even at 40 times earnings, the kind of multiple Nvidia trades around, the stock still doesn’t reach the top of management’s own grants. For those top strikes to pay anything, Meta has to earn far more than today’s math says it will. So the six people who read the real internal numbers every single morning just accepted pay packages worth zero unless the company blows past consensus. My own bull case tops out at $1,030 a share. They signed up for $3,500. Either they’ve lost their minds, or they’re counting on AI revenue I honestly can’t picture yet. They know this technology better than I do, so I know which way I’d lean.

What Could Go Wrong

Like everything I write, I’m coming at this from the buy side, and I’m biased toward great businesses. But there are real downsides here, so here’s the honest case against myself.

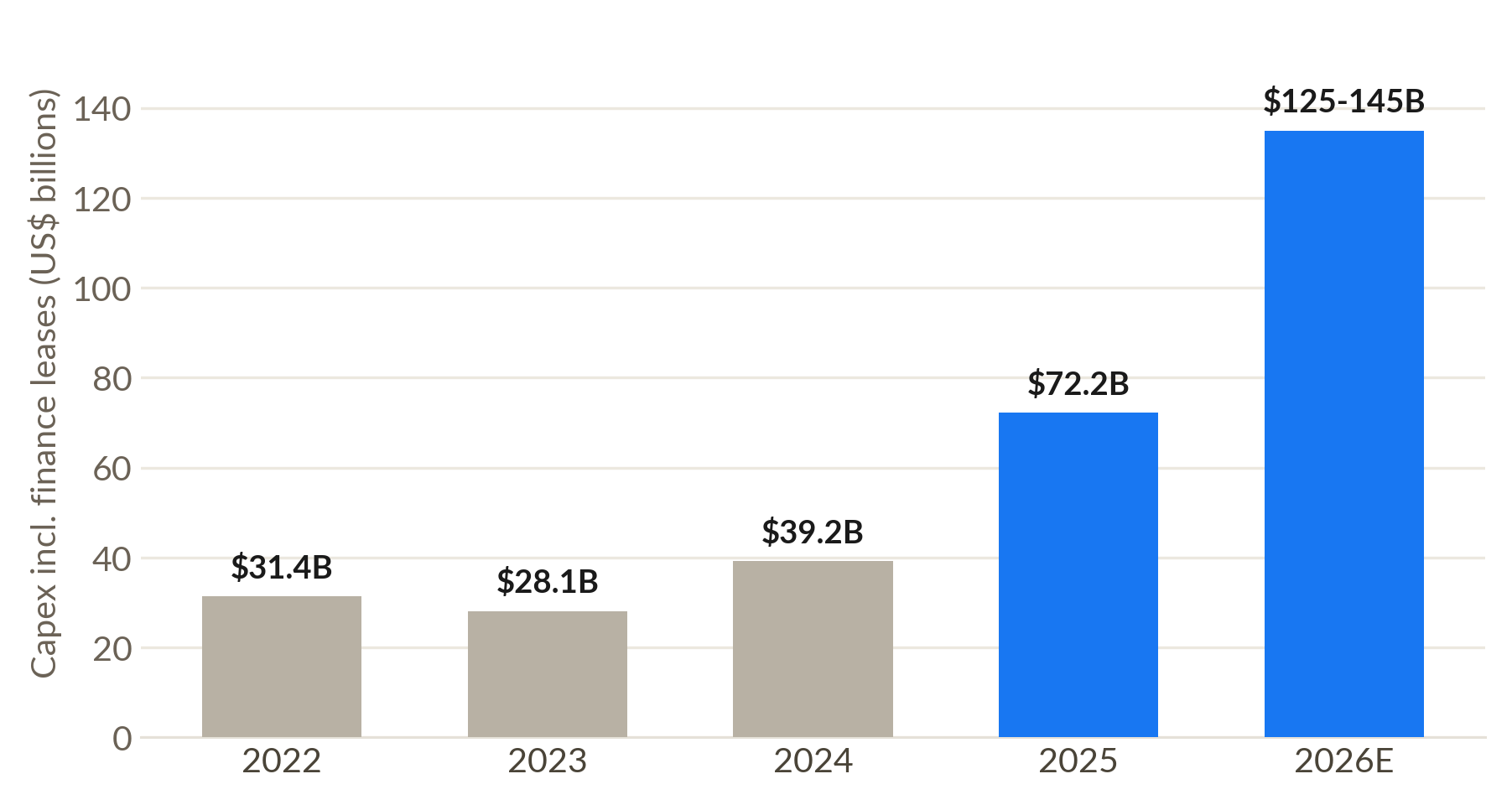

The real risk is the spending itself. Meta will spend $125 to $145 billion on capex in 2026, and all of it turns into depreciation over the next few years. If the AI doesn’t drive enough new revenue before that bill hits the income statement, margins get squeezed and the stock can go nowhere for a couple of years while earnings catch up. Meta is more exposed to this than Amazon or Microsoft, because it has no second engine. No AWS, no Azure, no outside customer paying for the compute. It’s one advertising business funding one enormous bet. The spending is so big that free cash flow could actually turn negative, which is a genuinely wild thing to say about a company that prints this much money. And the outside money is already flowing in: Meta sold $30 billion of bonds last October, the biggest US corporate bond deal of the year, and raised roughly $27 billion more off balance sheet with Blue Owl to finance its Hyperion data center. The equity-raise report that hit the stock on Friday is just the next step down the same path.

Figure 5: Capex has gone from $31B in 2022 to a guided ~$135B in 2026, more than free cash flow can cover, which is why the equity-raise report spooked people. Source: Meta filings; 2026 is the midpoint of $125–145B guidance.

But here’s why it doesn’t kill the company. This is the same Zuckerberg who, in late 2022, with the stock under $100 and shareholders in open revolt over the metaverse, cut 11,000 people, declared 2023 the “Year of Efficiency,” and then watched the stock run up roughly sevenfold. He course-corrected early and hard. Even with the stock in the gutter, he moved before the rest of tech would admit how badly they had all over-hired over the prior decade. I’m not rooting for layoffs, and they were brutal for a lot of people, but his ability to pivot that fast is genuinely rare. The catch is that AI capex isn’t as clean a pivot as the metaverse was, because the numbers are so much bigger. We’re talking about Meta pointing almost everything it has at this.

The second risk is antitrust, and this one is just my read, from someone who’s spent a fair amount of time around political circles. When the Democrats take back Washington, and they eventually will, I think Meta is near the front of the line, right alongside anything Elon Musk runs. The FTC, the Senate, and a president looking for a popular crusade could all turn their attention to it at once. This is a company with enemies on both sides of the aisle. (And it’s less settled than people assume. Meta won the FTC case last year, but the FTC appealed and 28 states plus DC are backing that appeal, so it’s pending, not dead.) All of that said, this is speculation and can’t be more than that. And even here the math probably cuts my way: forcing Meta to spin off Instagram wouldn’t destroy value, it would unlock it. It would finally put a real price tag on the $840 billion the conglomerate discount is hiding right now.

Conclusion

This is the easiest play I see. A money printer trading below 20x, where the apps alone are worth more than the whole company, where you get the AI bet for free, run by a founder who wastes money on the margins but has the cash flow to afford it and the track record to stop when it matters. If AI works, Meta leads. If it doesn’t, it stings for a while and then it’s back to printing money. One more time: look at the money they have.

All that being said, I think the base case is ~$690 a share on the apps alone, the bull case is ~$1,030, the downside is ~$425, and the upside nobody’s paying for is AI actually working. I’ll take that trade.

view all sources here

Suggested Citation: Rettke, Sterling. “$META: Is Everyone Overthinking?” sterlingrettke.com, June 9, 2026.

Disclosure: I own shares of Meta ($META) and am long the stock. This piece is for informational and educational purposes only and is not investment advice. Do your own research.

The content on this site is for informational and educational purposes only and does not constitute investment advice, financial advice, or a recommendation to buy or sell any security. Sterling Rettke is not a registered investment adviser. The author may hold positions in securities discussed. Always do your own research and consult a qualified financial advisor before making investment decisions.